Mastering ISOs (Incentive Stock Options)

A guide for advisors helping clients navigate AMT, avoid reporting landmines, and make equity feel manageable

There’s a moment that happens when ISOs “get real.”

This can be a milestone for the company (fundraising, tender offer, IPO) or a change in an individual's personal life (financial or tax situation, changing jobs, etc).

So they do what smart people do when something feels high-stakes: they open a spreadsheet.

And that’s usually where the trouble begins.

Because with ISOs, a spreadsheet rarely captures the three systems they’re actually dealing with:

- The equity plan system (what they can do, when, and under what rules)

- The tax system (regular tax vs. AMT)

- The reporting system (W-2s, 3921s, 1099s, Schedule D, Form 6251, Form 8801…)

Your client doesn’t need to become an equity comp expert to improve their after-tax outcomes, but they do need help from one.

The advisor/tax pro value comes from making ISOs feel navigable, reducing “surprise tax” risk, tying every decision back to the client’s goals, and helping everything get reported properly.

Below is the advisor-grade framework we teach for doing exactly that.

Why do ISOs create tax surprises even though they’re “tax-advantaged”?

Incentive Stock Options (ISOs) are designed to offer favorable tax treatment if the client follows certain rules. The potential reward is that, if certain conditions are met, an individual can purchase them without triggering tax and sell them at long-term capital gain rates.

But the nuance is a second tax system that clients often don’t know exists until it hurts: Alternative Minimum Tax (AMT). And even after feeling the pain, they still don’t understand it.

At exercise, ISOs can create an AMT “preference item” equal to the bargain element (spread), even though the client didn’t sell shares or receive cash. The increase in economic benefit doesn’t impact their paystub but can show up with an unexpected AMT bill at tax filing.

And if you want to be the hero in that story, you don’t start with the tax code. You start with the map.

Incentive Stock Options 101

What ISO terms actually matter for planning decisions?

The foundation for ISO confusion is vocabulary. Here are the terms that actually matter in client conversations:

- Exercise price (strike price): what the client pays per option they buy

- Fair market value (FMV): what the stock is worth at a point in time (for private companies, the 409A valuation)

- Spread / bargain element: FMV at exercise minus exercise price (× options exercised)

- Vesting schedule: when options become exercisable (if not early exercisable)

- Expiration / post-termination window: the last date a client has to exercise their options otherwise they lose them (post-termination is 90 days max, employer may convert to NSOs to retain original expiration date)

- Early exercise: exercising before vesting (if the plan allows it), which has hidden complications for ISOs

But when it comes to delivering value, ISOs are less about “what are they?” and more about when do we act, what does it cost, and what tax system are we triggering? These questions get to the “why” of the strategy, providing confidence and clarity.

The ISO Terrain: 4 moments, 2 tax systems, 1 client who just wants clarity

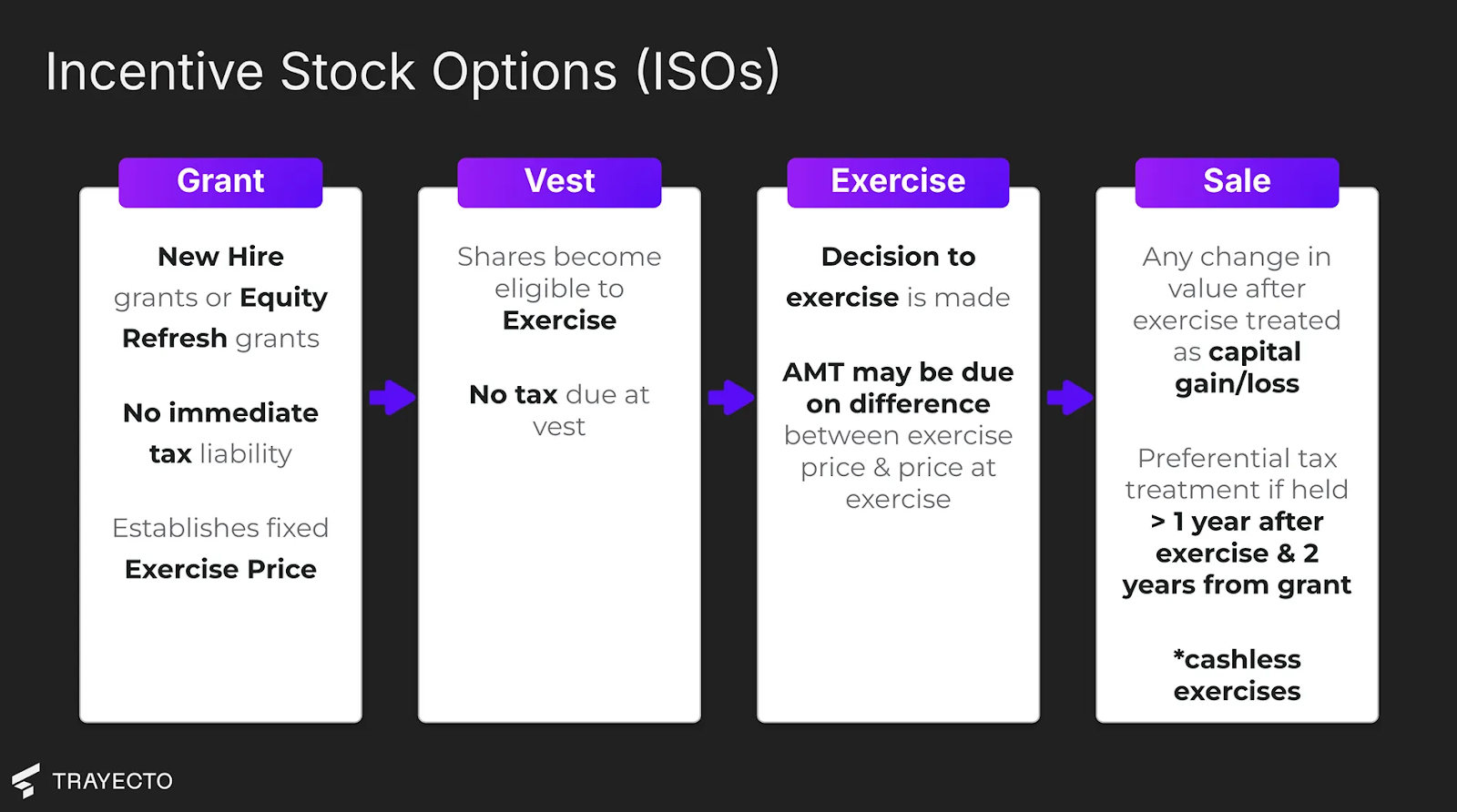

How do ISOs get taxed across grant, vest, exercise, and sale?

Here’s the practical timeline to anchor every ISO conversation:

- Grant (no tax)

- Vest (no tax)

- Exercise (AMT risk)

- Sale (capital gain and/or ordinary income)

The two moments that matter most for planning are exercise and sale—because that’s where the rules split into different outcomes.

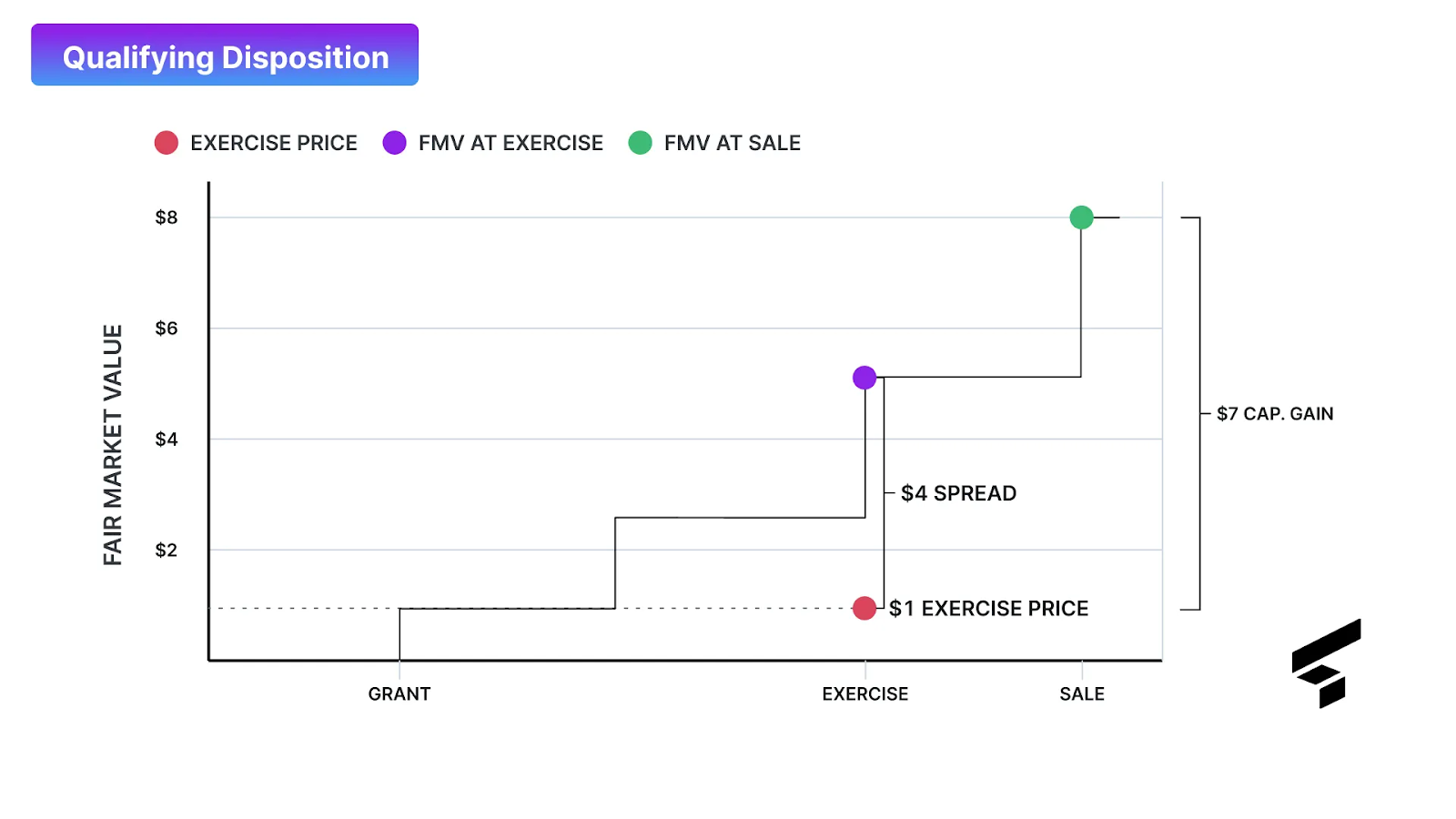

What are Qualifying vs. Disqualifying Dispositions?

The difference determines whether gains are taxed at long-term capital rates or ordinary income and short-term rates—and how AMT comes into play.

ISOs get their best tax treatment only if the client satisfies both holding period requirements:

- Hold shares at least 2 years from grant date, and

- Hold shares at least 1 year from exercise date

If they meet both: qualifying disposition.

If they fail either: disqualifying disposition.

What changes between the two?

In a qualifying disposition, the client gets long-term capital gains treatment on the difference between the sale price and the exercise price.

In a disqualifying disposition, the spread at exercise is treated as ordinary income and the additional appreciation above the FMV at exercise is a short-term capital gain (or loss).

A clean example you can reuse

Assume:

- Exercise price: $1

- FMV at exercise: $5

- Sale price: $8

Qualifying disposition:

- Spread ($4) matters for AMT tracking

- Sale price minus exercise price ($7) taxed as long-term capital gain

Disqualifying disposition:

- Spread ($4) taxed as ordinary income in the year of sale

- Sale price minus FMV at exercise ($3) taxed as short-term capital gain

A quick note about Disqualifying Dispositions is that someone may elect to exercise and hold initially, and then sell their shares in a future calendar year while still not meeting the conditions for a Qualifying Disposition. In this fact pattern, it’s possible to incur AMT in the year of exercise and in the year of sale pay short-term capital gain rates plus ordinary income on the spread.

Advisor framing: “Qualifying can improve tax treatment, but it also forces a timeline. The client’s real decision is whether the potential tax benefit is worth the concentration risk and holding period requirements.”

That framing keeps you out of “tax trivia” and inside “financial planning.”

What are the mechanics and tax implications of a Cashless Exercise?

A cashless exercise means exercising and selling simultaneously, using sale proceeds to cover the exercise cost. For ISOs, same-day sales create a disqualifying disposition outcome: the spread is treated as ordinary income, and any additional gain or loss is short-term.

When planning for a cashless exercise, you can assume the spread will be the difference between the sale price and the exercise price and that no capital gain or loss will be incurred. For publicly traded companies, the price at the time of exercise and the price at the time of sale may differ due to price movement that day, generating a small short-term gain or loss. After the transaction has closed and you receive detailed confirmation from the client, you can update your ledger (more on that later).

Why is AMT the invisible toll booth at exercise?

Because of our separate but parallel tax system, the client can do something that feels like “buying stock”… and the Alternative Minimum Tax system secretly accounts for the economic benefit received.

Here’s the simplest accurate explanation:

- For regular tax, ISO spread does not increase taxable income.

- For AMT, the spread is included as a preference item that increases the minimum tax liability.

A taxpayer only incurs Alternative Minimum Tax if the AMT liability exceeds the tax liability under the regular tax system. At which point the excess AMT shows up on the 1040 as an additional tax liability. (hence the name “Alternative Minimum Tax” system)

However, spread incurred on an ISO exercise only increases the AMT calculation if those exercised shares were still held as of 12/31 of the year of exercise. This is why the spread from a cashless exercise or a Disqualifying Disposition where the exercise and sale happen in the same calendar year does not impact the AMT system. In those fact patterns the spread would show up as ordinary income under the regular tax calculation.

Where is AMT calculated and tracked for ISO exercises?

AMT is calculated on Form 6251 and ISO bargain element data is reported on the Form 3921.

And here’s the piece clients almost never know (but you should):

If they pay AMT in one year, they may be able to recover some or all of it later through an AMT credit tracked on Form 8801. That credit can offset regular tax in future years where the regular tax exceeds the Alternative Minimum Tax, reducing the regular tax liability so they are equal. Unused credits are carried over until fully utilized or the taxpayer dies.

Advisor framing: “AMT isn’t a permanent cost, it can be recouped. But it becomes permanent if no one tracks it correctly or strategically plans for utilizing it.”

That’s not just technical expertise, it’s real money in the client’s pocket.

Form 3921: the “informational” form that quietly drives everything

What is Form 3921 and why does it matter for ISO planning?

When a client exercises ISOs, employers issue Form 3921. It includes the critical inputs you need for AMT and later reporting:

- Grant date

- Exercise date

- Exercise price

- FMV on exercise date

- Number of shares acquired

It exists to help track:

- The bargain element (spread) used for AMT calculations

- Cost basis details needed later when shares are sold

Here’s the nuance that matters for tax prep and AMT:

- A taxpayer may receive a Form 3921 for each exercise in a given year, rather than a single 3921 detailing each exercise transaction.

- A taxpayer may receive a Form 3921 for ISOs that were sold in the same year they were exercised.

Advisor move: don’t let your client, or their tax preparer, blindly “add up 3921 spreads” without understanding what was actually held at year-end.

Why might 3921 data not be included in a client’s tax return?

Form 3921 is often overlooked if the client, tax professional, and financial advisor aren’t communicating about exercise decisions.

When accounted for, there’s still a need to connect the dots across tax docs to ensure everything is reported correctly.

Advisor move: build an “ISO ledger” for the client once, using 3921 data and sale confirmations, and update it as they make decisions.

What is the ISO Reporting Trap?

Even when the planning is good, clients still lose money when reported incorrectly on the tax return. That’s because 1099-B forms frequently report incorrect cost basis, resulting in gains being overstated unless adjusted using 3921 data and supplemental reporting.

Why do ISOs have different cost basis for regular tax and AMT?

One of the most misunderstood aspects of ISOs is that the cost basis for exercised options may be different under the regular tax system and the AMT system.

In the regular tax system, ISO basis is the exercise price.

In the AMT system the cost basis is the FMV at exercise. Misreporting this is one of the ways clients pay higher than necessary tax and lose the opportunity to benefit from available AMT credits.

This difference becomes especially important when the client eventually sells shares in a qualifying disposition because they may have:

- Significant capital gains under regular tax, and

- Smaller gains under AMT due to the higher AMT basis, which can unlock AMT credit utilization.

Advisor framing: “AMT basis is why we track exercise history even if we’re not selling yet. It’s not busywork—it’s future tax savings.”

The documents that collide (and how to reconcile them)

When ISOs are sold, the sale appears on Form 1099-B. 1099-B includes proceeds and may include cost basis, but the cost basis is often incorrect.

That’s why custodians often provide a 1099 Supplemental, which includes specific adjustments to help correct the basis to avoid double taxation.

You can triple check the 1099-B and 1099 Supplemental with the 3921s and the “ISO ledger” outlined in the section above.

- Qualifying disposition: generally no cost basis adjustment required to the exercise price under the regular tax system. The AMT cost basis will be reported as the FMV at exercise, which is generally not reported on 1099s.

- Disqualifying disposition: the spread taxed as ordinary income must be reflected correctly as an adjustment to cost basis so that both tax liabilities are calculated correctly. If the disqualifying sale happens the year after exercise, there is additional nuance to address to ensure the tax return is correct.

Then everything rolls into:

- Form 1040 (ordinary income, capital gains, AMT, AMT credits)

- Schedule D (capital gains and losses)

- Form 6251 (AMT) and Form 8801 (AMT credits)

Disqualifying ISO ordinary income missing on the W-2?

Employers are not required to report the ordinary income from a disqualifying disposition on the Form W-2. And if it isn’t included, it may need to be reported as “Other income” on Form 1040 / Schedule 1.

Advisor move: ask for a copy of the client’s paystub after a cashless exercise occurs, if the wage income is not reported there be sure to account for it in your tax projection and make sure not to miss it on the tax return.

Advisor edge: a repeatable ISO playbook you can apply to every client

How can advisors and tax pros systematize ISO planning across clients?

Here’s the practical system your clients will feel immediately.

1) Build the “ISO ledger” once and update it as things change

Collect and organize:

- Grant documentation (exercise price, vesting, expiration, early exercise rights)

- Form 3921s (exercise history)

- Prior-year Forms 6251 and 8801 (AMT and credits)

- Brokerage 1099-B and 1099 Supplemental (sale history)

Advisor framing: “Our goal is to do forensic accounting to make sure we have an accurate history, inventory, and projections for your ISOs.”

2) Ask one question that determines the entire strategy

“Is the concentrated stock risk and holding period requirements worth the potential tax benefit of parting with money right now?”

That question clarifies whether the client is optimizing for:

- tax treatment, or

- their financial plan + cash needs

3) Model the AMT impact before acting

Use equity comp specific software, like Trayecto, or tax software to estimate whether exercising this year creates AMT and so how much.

Advisor framing: “We’re not guessing. We’re choosing the amount we can exercise with our eyes open.”

4) Pre-file reconciliation (the “no surprises” standard)

Before filing:

- Tie 3921 exercise data to AMT modeling

- Reconcile 1099-B with 1099 Supplemental so basis is right for capital gains

- Confirm whether disqualifying disposition ordinary income is on the W-2; if not, handle correctly

- Verify the form 8801 is accurately tracking AMT credits

This is where you save clients from paying tax twice, missing AMT credit utilization opportunities, or from getting the dreaded IRS notice.

5) Tie ISO decisions to goals (not just taxes)

Clients don’t improve their after-tax outcomes because they memorized holding period rules. They win because you connect equity decisions to life:

- building a cash buffer before leaving a job and dealing with expiration dates

- reserving cash for estimated payments

- funding a home down payment

- diversifying away from single-stock risk

- deciding how much of a tender offer to participate in

That’s where you become indispensable. Not because of value at a given point in time, but because of the continuity of guidance you can provide and your ability to simplify the complexity.

With this in-depth understanding of ISOs, you can apply this knowledge to any ISO-related situation your client is dealing with - whether it’s a public or private company.

Final thoughts

ISOs aren’t “complicated” because the math is hard.

They’re complicated because clients are making irreversible decisions at moments of uncertainty—job changes, liquidity events, market volatility—while three different systems (plan rules, tax rules, and reporting rules) collide.

The advisor/tax pro who can calmly quarterback that collision becomes the hero of the story: fewer surprises, fewer mistakes, and a strategy the client can actually follow with confidence.

Related guides: