Mastering RSUs (Restricted Stock Units)

A guide for advisors helping clients navigate equity, avoid tax surprises, and optimize outcomes.

Even when RSUs seem “simple,” they can be a planning minefield for clients and an opportunity for advisors to demonstrate value. From surprise tax bills to misreported income, RSU events often surface confusion, emotion, and urgency. That’s where you step in.

This guide explains the key differences between single-trigger and double-trigger RSUs and shows how proactive advisors help clients:

- Identify costly underwithholding and double taxation

- Build liquidity strategies around vesting events and trading windows

- Confidently plan for taxes, timing, and long-term goals

What are RSUs and when do they become taxable?

Restricted Stock Units are not actual shares. They represent a promise to deliver company stock in the future once certain conditions are met.

When those conditions are satisfied, RSUs convert into stock and trigger ordinary income taxation based on the fair market value (FMV) at that time.

The type of RSU determines when income is incurred and when tax withholding is due, which is where planning differences begin.

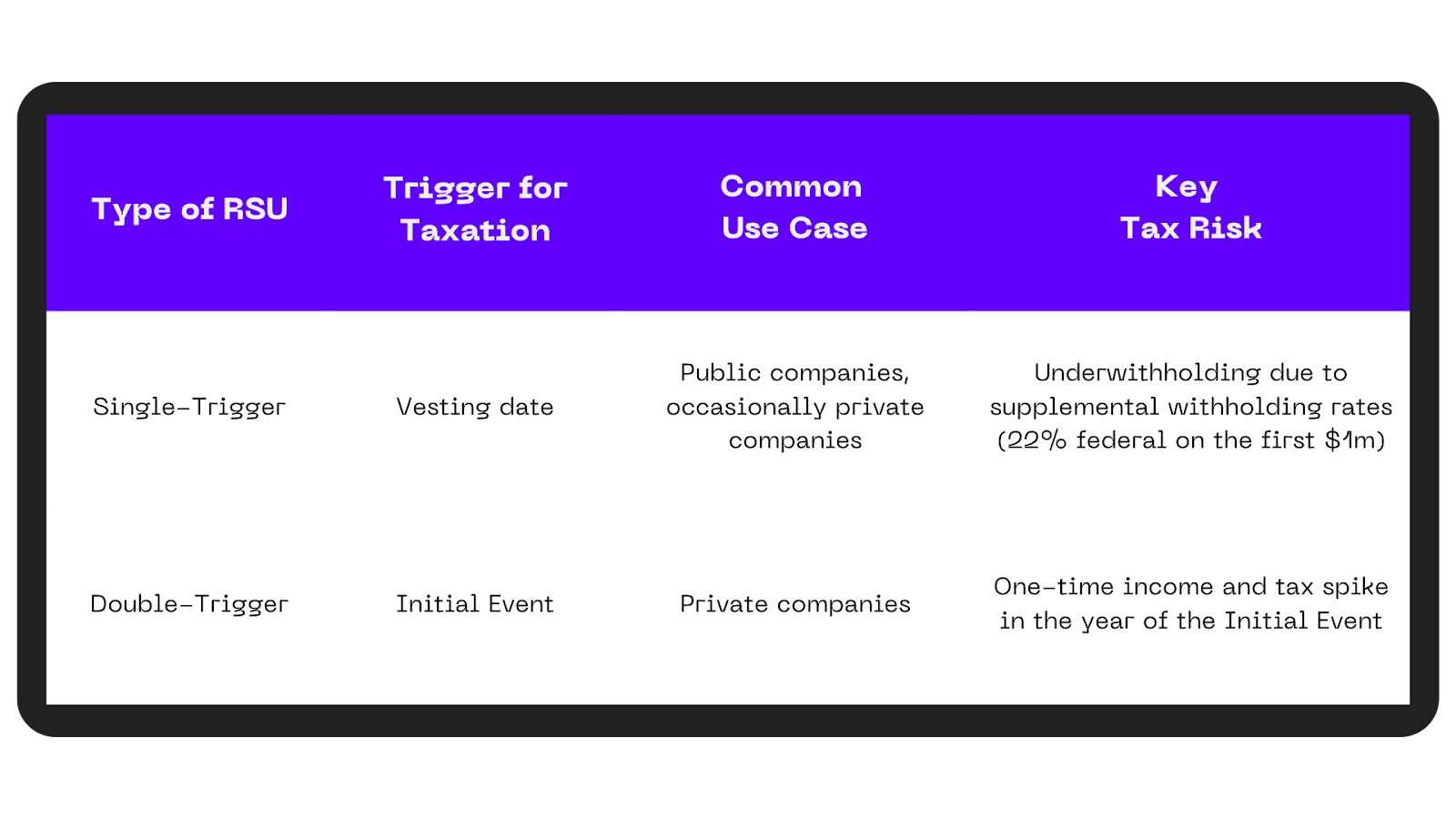

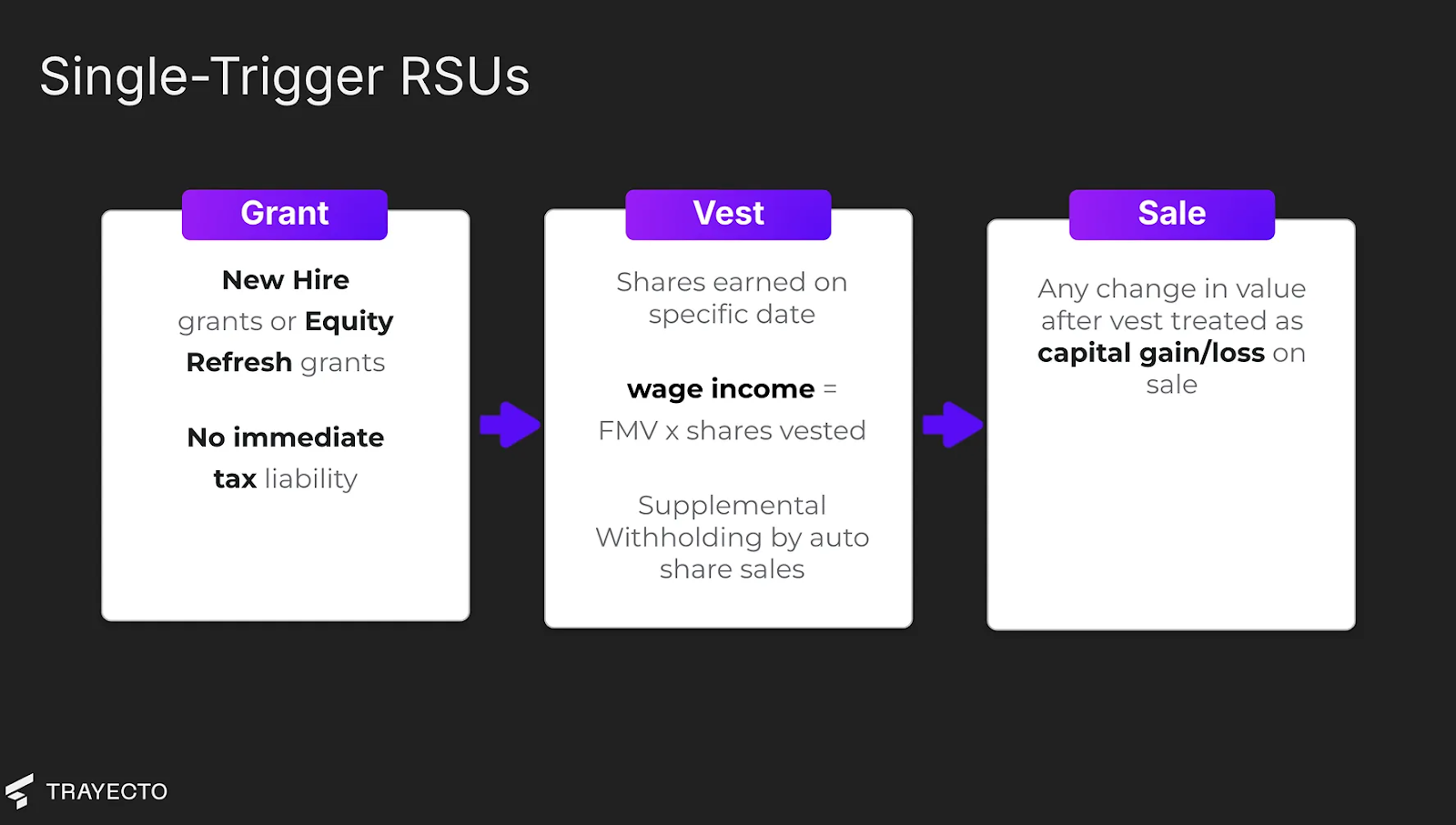

How do Single-Trigger RSUs work and why do they often cause surprise tax bills?

Single-trigger RSUs are taxed as ordinary income at vest, and automatic withholding often falls short of a client’s true tax liability.

For Single-Trigger RSUs no tax is due on grant, the taxable income is incurred on vest date. Once the shares vest, the FMV multiplied by the number of RSUs vesting is treated as supplemental wage income. Supplemental income requires automatic withholding at supplemental tax rates, which is typically covered by selling shares on vest. Supplemental wage income is subject to 22% withholding at the federal level (increases to 37% above $1m of supplemental income in a calendar year), plus Social Security, Medicare, Medicare Surtax, and a flat state supplemental wage rate.

Key Advisor Considerations:

Why is RSU withholding often lower than a client’s actual tax liability?

RSU income withholding rates are often below clients’ effective tax rates because of other wage income from salary and bonuses. It’s also common for w-4 withholding on the paystub to be below their effective tax rate as well. That cumulative mismatch leads to underwithholding and a surprise tax bill because each dollar withheld is below the rate needed to fully cover the tax liability. Without guidance it can be difficult for clients to understand how RSU income and withholding connects to the rest of their fact pattern.

Some employers allow clients to adjust the federal withholding percentage on a per-grant basis (e.g., 30%, 32%, or 37% for all vests even if below the $1m threshold). This means more shares are automatically sold on vest. This can be a convenient way to cover tax underwithholding without impacting recurring cash flows from paystub withholding. This also ties the sale price to the vest price, mitigating the chance that shares need to be sold at a material loss at the next trading opportunity relative to the price at which they incurred supplemental wage income.

If a client cannot adjust their federal withholding on RSUs, the delta will need to be covered another way: cash on hand, accumulated excess cash flows, or selling assets (like their company stock).

How is RSU income reported and how clients can accidentally pay tax twice?

RSU income is reported as wages on the W-2 and share sales appear on the 1099-B, often with missing or incorrect cost basis, which can lead to double taxation if not reconciled.

RSU income shows up in Box 1 of the W-2 and is specifically itemized in box 14, while the corresponding withholding shows up in the respective tax withholding boxes along with the withholding on other wage income.

Sales show up on the 1099-B, typically with a $0 cost basis and indicated as “cost basis not reported to the IRS”. Without a 1099 Supplemental showing the correct cost basis, clients risk double taxation when filing the return (first as wages, then again as capital gains with $0 basis). Advisors can help prevent this by proactively reviewing tax documents and tax returns before their client files.

When does the capital gains clock start for RSUs?

For single-trigger RSUs, the holding period starts on the vest date, not the grant date.

While some clients hold for 12+ months to capture long-term tax alpha, it’s not always worth the risk. A single stock can easily fluctuate by more than the difference between short- and long-term capital gains rates over that timeframe. It’s important to anchor the sale decision and benefits of tax optimization to the client’s cash needs and time horizon - like estimated tax payments to mitigate penalties and interest on underwithholding.

How does state tax withholding complicate RSU planning?

State supplemental withholding rates differ from federal rates - each state has its own flat rate. When RSU vesting is combined with other aspects of a client’s fact pattern, this will influence their taxpayer experience.

The context above about paying tax twice at the federal level also applies to the state.

Double-Trigger RSUs: Waiting for Liquidity

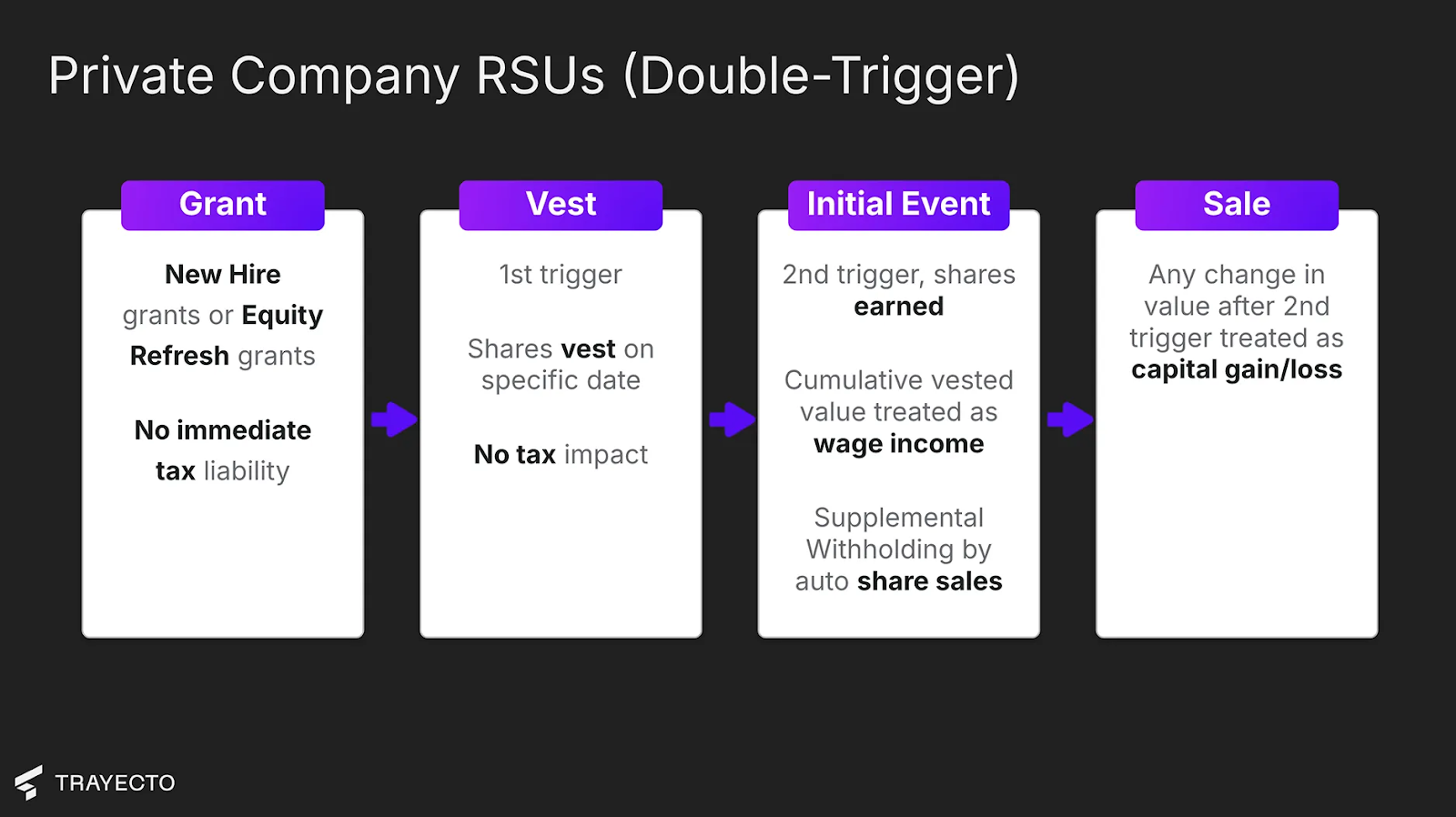

What makes double-trigger RSUs different from single-trigger RSUs?

Double-trigger RSUs require both vesting and a separate liquidity or transaction event before they become taxable.

At private companies, RSUs often have a second trigger (the “Initial Event”) that must occur in addition to vesting before taxation applies. This Initial Event is usually tied to acquisition, IPO, or an employee’s ability to transact. Until that event, the units are an unfunded liability for the company to provide shares to the employee.

What Triggers Taxation for Double-Trigger RSUs?

Tax is triggered only after both time-based vesting and the Initial Event occur, at which point all previously vested units become taxable at fair market value on the Initial Event date.

- Time-Based Vesting (Trigger 1) — shares vest, but no tax is owed

- Initial Event (Trigger 2) — all previously vested shares convert and become taxable at the FMV on the trigger date

After the initial event, any unvested double-trigger RSUs are treated as single-trigger RSUs upon vest.

Key Advisor Considerations:

What risks do advisors need to watch for with double-trigger RSUs?

Expiration Risk

Double-trigger RSUs usually come with expiration dates. If the Initial Event DOES NOT occur before the deadline, the client could lose the entire value because the unfunded liability is not converted into shares. Most clients aren't aware of this and few companies make it obvious in grant summaries, it’s often buried in the legalese of the grant document. Advisors can help by reviewing equity plan docs and surfacing these timelines.

Lump-Sum Tax Liability on Initial Event

Upon the Initial Event, all previously vested RSUs become taxable all at once at the FMV. Even if some shares are withheld at 37%, the first $1,000,000 in RSU value would be underwithheld at 22%. Clients can face mid-six-figure tax bills with limited time to sell stock before payment is due.

Grant-by-Grant Withholding Adjustments

Some companies allow pre-IPO (or pre-Initial Event) employees to increase the withholding rate on RSUs by submitting updates before a deadline This must be done per-grant and ahead of the trigger. A missed window means a missed opportunity.

Issuance Timing & Lockups

When a company goes public, the IPO date may or may not be the Initial Event. The Initial Event, and first open trading window, must happen by the earlier of 7 months post-IPO or March 15th of the following year. Advisors can forecast this timeline and help clients prepare a cash cushion or sale strategy that aligns with lockup expirations and tax payment deadlines.

When does the capital gains holding period start for double-trigger RSUs?

The holding period for capital gains starts on the Initial Event date, not the vest date. This establishes the timeline for long-term treatment even for shares vested in years prior.

Advisor Edge: Turning RSUs Into Planning Wins

How can advisors turn RSUs into planning wins instead of tax headaches?

Advisors create the most value with RSUs by anticipating tax outcomes, coordinating liquidity, and reconciling reporting before mistakes happen. In short - it’s all about expectation setting and articulating trade-offs of potential next steps.

To go beyond the basics, use RSU events as strategic entry points. The goal isn’t just minimizing taxes, it’s building confidence and clarity into your client’s bigger picture.

- Model Withholding Scenarios Instantly: Use Trayecto or other tools to project total RSU income and compare actual withholding to the client’s effective tax rate. This reveals potential underpayment before it turns into a penalty and gives the client time to plan for payments.

- Time Sales with Tax Deadlines and Other Liquidity Needs: Help clients sell shares during open trading windows to fund upcoming estimated payments and future spending needs. If clients qualify for the safe harbor rule, you can provide guidance so they earn interest in a high yield savings account until tax must be paid.

- Avoid Reporting Errors with Full Document Review: Reconcile W-2 income, 1099-B transactions, and the 1099 Supplemental to avoid basis errors and double taxation. Advisors who can proactively address this add immediate, tangible value and reduce IRS notice headaches.

- Coordinate with Cash Flow & Goals: RSUs shouldn’t exist in a vacuum. Use Trayecto to map equity events against life milestones: home purchases, tuition funding, debt payoff. This is how you turn episodic equity into holistic planning.

Final Thought

Just because RSUs are common and “simple” doesn’t mean you can’t add value or clients don’t deserve in-depth analysis. Helping clients avoid tax shocks, address reporting issues, and fund their goals transforms equity into empowerment. For advisors who want to stand out in the tech niche, mastering RSUs is the table stakes.

If you don’t have access to software that helps you streamline RSU planning, request a demo of Trayecto.

Related guides